1. Looking back on 2022, demand is sluggish, supply is shrinking, and the industry is bottoming out.

1. Among them, float method is to float glass on the surface of tin, using surface tension, gravity and mechanical pull to form, which is the production mode with the highest production capacity at present, and the downstream is mainly used in real estate, automobiles, household appliances and other fields. Among them, the real estate sector accounts for 85%, which is the main market affecting glass demand. After 2015, with the implementation of supply-side reform and capacity replacement policy, the new production lines of float glass were significantly reduced, and the supply was mainly affected by the number of cold repair and production lines. The calendering method is to roll the molten glass through the calendering roller, and the embossed glass can be produced by engraving patterns on the calendering roller, which is mainly used in the field of photovoltaic glass. At present, the state does not require capacity replacement policy for new production lines of photovoltaic glass, and calendering capacity is growing rapidly with the outbreak of demand for downstream photovoltaic modules.

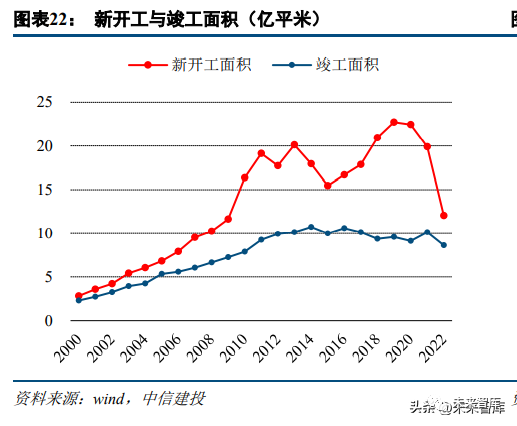

The glass installation is in the later stage of the real estate construction process. It takes about 15 months from the commencement of the project to the installation of the glass exterior wall (affected by the floor height), and about 4 months from the installation of the exterior wall to the completion. Theoretically, the growth rate of the new construction area and the completion area should be the leading and lagging indicators of the growth rate of the glass demand respectively.

In 2022, real estate investment and construction were under obvious pressure, and the growth rate was at a historic low. According to the data of the Bureau of Statistics, since 2022, the cumulative year-on-year growth rate of new housing construction area has gradually declined, and the annual new housing construction area has decreased by 39.4% to 12. The speed of real estate land acquisition has declined sharply, making the growth rate of land acquisition area decline to a historical low, and the new housing construction area is expected to continue to decline in the future. The area of land purchased in 2022 decreased by 53.4% year-on-year to 1.

1. Glass prices rose slightly in the first half of 2022, although they began to decline after March, but glass enterprises are optimistic about the demand in the second half of the year, combined with the sufficient cash flow accumulated in the last cycle, the number of cold repairs in the industry in the first half of the year is small, only 10; Since the second half of the year, with the continuous shrinkage of real estate demand, the "golden nine silver ten" of the glass industry has not yet appeared, and the industry has suffered obvious losses. Glass enterprises, especially small and medium-sized enterprises, have launched cold repair plans, with 32 cold repairs in the second half of the year. From 2018 to 2021, the annual number of cold repairs in the industry remained at about 15, and the scale of cold repairs in 2022 increased significantly compared with the past five years. In the downward cycle stage of the

glass industry in 2022, the number of new production lines has been significantly reduced, and the total capacity of the industry has contracted significantly. In 2022, only 2 new production lines will be built and 14 production lines will be resumed, with a total capacity increase of 12,300 t/d; 2. Float glass production capacity began to decline rapidly in the second half of 2022, and by the end of 2022, the industry's production capacity was 158300 t/d, down

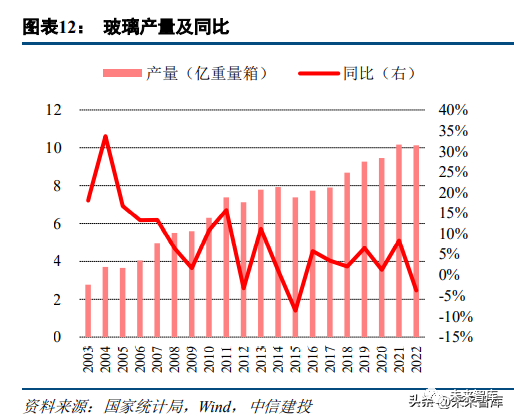

from the same period last year. In 2022, the annual glass output grew negatively for the first time in seven years. In 2022, the national glass output was 1.012 billion weight boxes, a decrease of 3. In the first half of 2023, the national glass inventory showed an upward trend, from 40 million weight boxes at the beginning of the year to 80 million weight boxes; Since the second half of the year, with the contraction of the supply side, the inventory has declined, and now it is about 65 million weight boxes, and it is in the situation of continuous inventory reduction.

1. At present, natural gas, heavy oil, petroleum coke, coal gas, coal tar and other fuels are widely used in domestic production lines. Among them, natural gas, as a clean traditional energy, is mainly used in middle and high-end production lines, and its proportion is increasing with the trend of environmental protection. Heavy oil fuel has high calorific value and almost no ash, which is convenient for automatic operation. Petroleum coke is a by-product of refinery coking unit, and its high iron content will cause the reduction of glass transmittance; Coal gas is mainly used in Hebei Province, which will produce dust and nitrogen sulfide pollution in the combustion process, and will be gradually replaced by natural gas production line in the future. Coal tar is a by-product of coal coking process, and it is also necessary to pay attention to nitrogen sulfide pollution. Raw materials mainly include soda ash, quartz sand, limestone, dolomite, feldspar, etc. Because the particle size of heavy alkali matches with quartz sand, in order to improve the uniformity of raw material mixing and reduce the erosion of sodium chloride in soda ash on refractory materials, heavy alkali is generally used as raw material for float glass. In addition, according to the special properties of the product, clarifiers, colorants, decolorants and other auxiliary raw materials will be added.

At present, all kinds of fuels in China's glass production line have a certain share, and the trend of "coal to gas" will continue in the future. At present, the proportion of production lines using natural gas as fuel in China's glass industry is about 40%, using coal gas as fuel is about 24%, and using petroleum coke as fuel is about 16% . In terms of fuel selection, enterprises should first consider the stability of supply, for example, northern China is rich in coal resources, and in the past, most enterprises chose coal gas or coal tar; second, based on the requirements of glass quality, for example, ultra-white glass and automotive glass are of high quality, and natural gas is generally used for production; Thirdly, we should consider the requirements of environmental protection policies, such as building and renovating production lines in North China to gradually realize the substitution from natural gas to coal fuel.

Among the raw materials, the cost of soda ash accounts for the highest proportion, and the demand for quartz sand is the largest. The price of quartz sand per ton is relatively low and the fluctuation is relatively small, which has limited impact on the glass production cost, while soda ash accounts for the largest proportion of raw material cost, and the market price fluctuation is also large, which will significantly affect the glass production cost, and then affect the glass price. The prices of

natural gas, petroleum coke and other fuels showed an upward trend in 2022. In 2022, affected by the international environment, energy prices continued to rise, and the price of liquefied natural gas in China rose from 3.3 yuan/cubic meter at the beginning of the year to the highest 5. In actual production, most of the natural gas in glass enterprises comes from pipeline gas, and the price varies from region to region. However, in the period of tight supply, it will also be supplemented by the purchase of LNG. In addition, the price of pipeline gas is also affected by the price of LNG in the international market to a certain extent.

glass industry has suffered overall losses, with profits at the lowest level in recent years. Although the current price of glass is basically the same as that in 2019-2020, the price of natural gas, petroleum coke and soda ash at the fuel end has increased significantly compared with that in 2019-2020, so the profitability of the glass industry is significantly lower than that in the past, and the profits of different fuel production lines at the industry level have suffered losses.

2. Looking forward to 2023, the downward space is limited, and the upward elasticity is mainly affected

by demand. 2. Since 2018, there has been a significant deviation between the new housing construction and the completed area. Even with the negative growth of real estate investment and the new construction area in 2022, there is still a large stock of the area to be completed. In 2022, the completed area decreased by 15% year on year due to factors such as the epidemic situation and the funds of real estate enterprises.We judge that the ratio of completed area to theoretical completed area in 2023 is expected to increase. Generally, the new construction index is about two years ahead of the completion index. We define the new construction area in the first two years as the theoretical completion area.

By calculating the ratio from 2005 to 2021, it can be found that from 2005 to 2011, the statistical completion area/theoretical completion area is basically maintained between 80% and 100%, and the fitting relationship between them is good; Since 2012, the ratio has dropped sharply, from 79.78% in 2011 to 60.76%, and remained in the range of 50% -60% in the following seven years; Since 2019, the ratio has entered the downward range, with 43.57% in 2020 and 44.2023 in 2021, respectively. The basic trend of the completed area in 2023 is similar to that in 2016. The real estate support policy has been introduced intensively, and the pre-construction area has declined. It is expected to bring about a rebound in the proportion of completed area to theoretical completed area.

Under the above assumptions, we expect that the completed area will rise in 2023. Assuming that the ratio of statistical completed area to theoretical completed area is pessimistic, neutral and optimistic, the neutral assumption is that the ratio will rise to 44.11% of the average level in 2020 and 2021 in 2023; Optimistic assumption: in 2023, the ratio will accelerate to rise to the average level of 47.31% in 2019-2021; Pessimistic assumption: In 2023, the ratio will remain at the expected level of 38 in 2022. Therefore, we can conclude that in the optimistic/neutral/pessimistic case, the completed area in 2023 will be 940, 877 and 764 million square meters respectively. The year-on-year growth rates were 9.13%, 1.75% and -11% respectively.

Glass sales growth indicators were generally about 4-6 months ahead. Based on the inventory and output data of each month, we calculate the sales data of glass in each month, and compare the growth rate of glass sales in each month with the growth rate of completed housing area. It is found that the growth index of glass sales is generally 4-6 months ahead of the growth index of completed area, but due to the difference of inventory stock between intermediate distributors and deep processing enterprises, there are deviations in the fitting degree of some months.

From the monthly distribution of the completed area, the completion is concentrated in December. According to the monthly completion area index in previous years, the fourth quarter, especially December, is the time for centralized completion. Taking the data of the past five years as an example, the completion area in the fourth quarter accounts for 50.65% of the annual completion area, and the completion area in December accounts for 32% of the annual completion area. The projects completed in the second half of the year are basically the purchase and installation of glass in that year. From the perspective of annual demand forecast, it is more realistic to use the completed area of the year to forecast the glass demand of the year.

By analyzing the historical data, it is found that the glass production capacity has a high correlation with the completed area in that year. From 2018 to 2021, the average proportion coefficient of annual glass production capacity per 10000 square meters of completed area is 1. According to this calculation, the growth rate of completed area in 2023 is -20%, -10%, 0%, 10% and 20%. The corresponding glass production capacity demand is 11.80, 13.27, 14.74, 16.22 and 17 respectively. The current glass production capacity is about 15.2

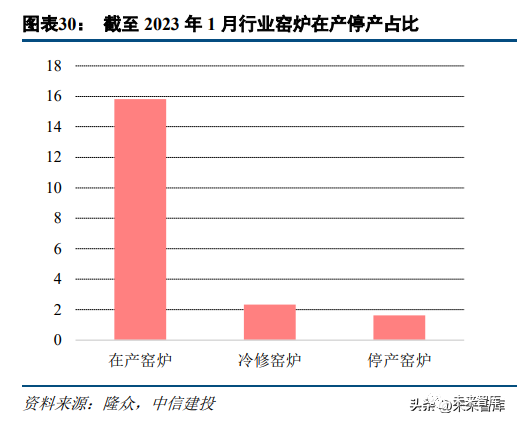

. By the end of January 2023, the industry is producing 158,300 t/d of kilns and 23,300 t/d of cold repair. Shutdown of kilns 1. At present, the capacity utilization rate of the industry is less than 80%. Since the implementation of the supply-side reform and capacity replacement policy in the glass industry in 2015, the total capacity of the glass industry has entered a stable stage of development, but there are still some production lines for kilns in 2014 and before, and 17.40% of the kilns are 9-10 years old. Production capacity of more than 10 years 9. Because the refractory materials of the glass production line will be gradually damaged over time in the production process, and the impurity layer will precipitate at the bottom of the glass liquid pool year by year, the fuel consumption will increase, the glass melting capacity will decrease, and the cost will increase. Therefore, the operation cycle of the general glass furnace is 8-10 years. After that, relevant equipment and materials shall be replaced by cold repair. According to the statistics, the total production capacity of kilns in production for more than 9 years is 4.

Through the analysis of cold repair kilns, the proportion of cold repair production line to resume production is low. Under normal circumstances, the enterprise will select and order refractory materials and related equipment half a year before the planned cold repair period. After entering the cold repair period, it will take about half a year to complete the production line renewal and meet the conditions for resumption of production. In 2022, due to the continuous decline in glass prices, a large number of production lines were passively cold repaired due to losses. According to statistics, in cold repair kilns, the proportion of production capacity over 8 years is only 36.47%, and the proportion of production capacity under 6-8 years and 5 years is 24.24% and 39. On the one hand, the preliminary work of cold repair in passive cold repair production lines is generally not carried out. On the other hand, due to the shortage of funds, some production lines are "cold but not repaired". Therefore, it is expected that the proportion of the cold repair production line resuming production in 2023 will not exceed 50%; in addition, most of the cold repair kilns are concentrated in the third and fourth quarters of 2022, so the actual production capacity contribution of the kilns resuming production in 2023 is not high. In

2023, the production capacity of the glass industry will be affected by demand fluctuations. In the optimistic scenario, the demand for glass is strong, the cold repair of the production line with a kiln age of more than 10 years is delayed, and the production line with a kiln age of more than 10 years is planned to resume production in 2022, with a total capacity of 166,800 t/d; in the neutral scenario, the production line with a kiln age of more than 10 years is planned to be cold repaired, and the production line with a kiln age of more than 10 years is planned to resume production in 2022, with a total capacity of 152,000 t/d; Under the pessimistic scenario, the cold repair of production lines with kiln age of 9 years or more, the delayed resumption of production of cold repair production lines in the 2022 plan, and the lower limit of total production capacity 11.2

. The unit price of each fuel and raw material at different times is used to calculate the production cost of the glass industry in each period. By comparing with the current glass market price, the average gross profit rate of the glass industry in different periods can be calculated to show the industry cycle law.

(3) 2015-2019: the implementation of capacity replacement policy, the start of supply-side reform in the glass industry, the expansion of production capacity into a steady growth stage, the gross profit margin of the industry increased to 20%, although the pace of completion and delivery slowed down after 2018, the demand has weakened, but in the context of capacity constraints. The gross profit margin of the glass industry has fallen significantly lower than that of the previous two cycles. (4) 2019-2022: Since 2019, the peak of cold repair and completion of the industry has gradually arrived, the industry has been in short supply, the price has risen sharply, and the gross profit rate once exceeded 50%; In 2022, the financial pressure of real estate enterprises increased, the completion structure slowed down significantly, the annual growth rate of completed area was -15% year-on-year, and the gross profit rate of the industry returned to the low level in 2014.

Through the review, we found that the cycle trend can be judged by the relative change of the completed area and the industry output. The law of the two cycles can be explained by comparing the monthly cumulative output growth rate and the cumulative completed area growth rate of glass from 2015 to 2019 and from 2019 to 2022. Looking forward to 2023, although the demand side has experienced turning point since August 2022, it is difficult to promote the price upward because the glass production is still at a high level and the actual completed area is still at a low level. However, by the end of 2022, the glass production has dropped significantly, the glass inventory has begun to decline, and the bottom of the price has rebounded.

Through the recovery cycle, we believe that the glass industry is expected to usher in an upward cycle in 2023, and the increase in gross profit margin will be directly affected by the downstream completion demand. (1) If the demand growth rate continues to be weak in 2022, the industry still needs further cold repair to shrink production capacity, the gross profit rate will fluctuate at 0%, and the glass price will be about 1776 yuan/ton when the raw material and fuel prices remain high in 2022 (high cost scenario). When the price of glass raw materials and fuel falls back to 2020 (low-cost scenario), the price of glass is about 1421 yuan/ton. (2) If the growth rate of completed area recovers to 0% -10% and the current supply and demand are basically balanced, the gross profit rate of the glass industry is expected to recover to the average level of 2016-2018, which is about 20%, and the glass price will rise to 2220 yuan/ton and 1777 yuan/ton respectively under the scenarios of high cost and low cost.(3) If the growth rate of completed area exceeds 10%, the glass industry will be in short supply, the gross profit margin of glass price is expected to reach 40%, and the glass price will rise to 2960 yuan/ton and 2369 yuan/ton respectively under high cost and low cost scenarios. At present, the average price of glass is 1660 yuan/ton, and there is a lot of room for growth in the future.

3. Analysis of

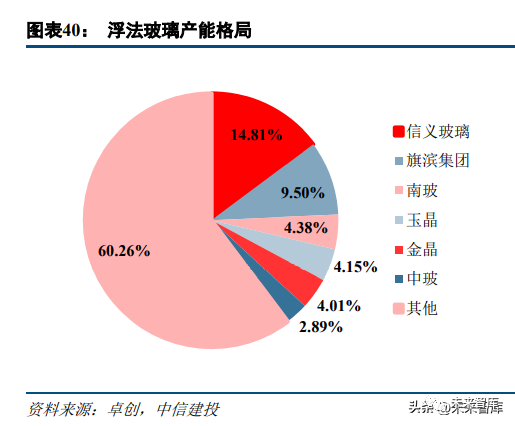

key enterprises 3. The first echelon is Xinyi Glass and Qibin Group, with production capacity of 28200 t/d and 18100 t/d respectively. The two leading companies have many bases in China and overseas. In 2021, the float glass business revenue of the two companies was 17.912 billion yuan and 124 yuan respectively.

The gross profit margin of the leading companies was significantly ahead of other companies, and the future industry structure is expected to be further optimized. At present, the production capacity of Xinyi Glass and Qibin Group accounts for 14.8% and 9% respectively. There are three reasons: the first is that the float glass technology is relatively mature and the production line rises earlier; the second is that the downstream demand for float glass is relatively dispersed, while the downstream demand for photovoltaic glass is mainly concentrated in the southeast coastal areas, which is conducive to the formation of large-scale production lines and enterprises; The third is the rapid growth period of photovoltaic glass demand after 2018, when China has started supply-side reform, the approval of energy consumption indicators for high energy-consuming production lines is more stringent, and the leading enterprises are more likely to obtain indicators to increase market share.

For the float glass industry, the gross profit rate of leading enterprises is more than 10% higher than that of the second echelon all the year round, which has become the core competitiveness of its ability to cross the cycle. In the past few years, Xinyi Glass acquired Walrun's production lines and related indicators in Zhangjiagang, Jiangsu and Jiangmen, Guangdong from 2018 to 2020, and signed the Restructuring Investment Framework Contract with AVIC Tebo in 2020, adding four production lines to Hainan Base and further expanding its production capacity; Qibin Group merged and reorganized Zhuzhou Glass Factory in 2005 and entered the float glass industry; it acquired Zhejiang Glass in 2013 and became the second largest float glass enterprise in China. We believe that under the restriction of capacity replacement policy, the total capacity of the industry will remain stable. In each downward cycle, some enterprises' production lines will withdraw from the market due to poor management, and leading enterprises are expected to further increase their market share in this process.

By sorting out the situation of cold repair and resumption of production lines of leading enterprises in 2022, we can see that the rhythm of cold repair of leading enterprises is basically not affected by the industry cycle. From the perspective of the kiln age of cold repair production lines, the kiln age of most cold repair production lines of the two companies has reached 10 years, which belongs to the planned cold repair; Xinyi Hainan Line 2 and Pengjiang Line 2 are the technological upgrading of production lines after the acquisition of Walrun and AVIC Tebo in 2020, so the kiln age is relatively short. A total of three production lines in Qibin will resume production in 2022, and the cold repair time of these three production lines is only 4 months, 6 months and 5 months respectively, which also shows that these three production lines are planned cold repair.

3.2 Qibin Group

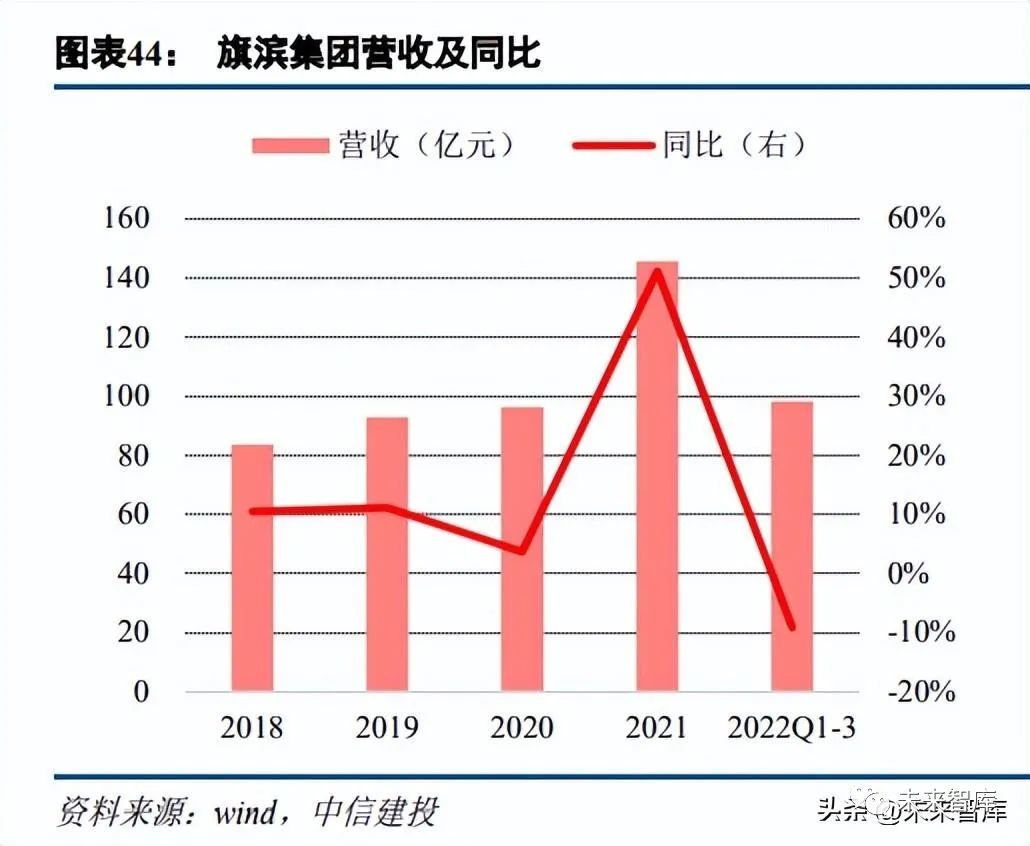

Qibin Group is one of the leading float glass enterprises in China, accounting for the proportion of production capacity. 9. The Company acquired the glass assets of Zhuzhou Guangming Glass Group in 2005 to enter the glass industry, and acquired Zhejiang Glass in 2013, becoming the second largest float glass enterprise in China. After more than ten years of development, the company has actively expanded energy-saving building glass, photovoltaic glass, electronic glass, pharmaceutical glass and other fields on the basis of float glass, and its scale has continued to grow. In 2021, the company's revenue reached 14 billion 573 million, an increase of 51.13% over the same period; The net profit attributable to the parent company was 4.234 billion yuan, a year-on-year increase of 133.2022. Affected by the weak downstream demand, the glass price continued to decline, and the company's performance was under short-term pressure. In the first three quarters of 2022, the company's revenue was 9.839 billion yuan, a year-on-year decrease of 9.09%; Net profit attributable to parent company was RMB1.249 billion, representing a year-on-year decrease of 66.

Qibin Group mainly engaged in the production of float glass sheets, accounting for 85% of its performance in 2021. In addition, the company has actively expanded its deep processing business, and the proportion has increased year by year, from 7.19% in 2019 to 13% in 2021. The gross profit rate of the company's original film business is greatly affected by the market price. The gross profit margin of float sheet fell below 20%.

(1) Original film and deep processing business

The company has a number of production bases in the southeast coast and overseas areas. At present, the company has float glass bases in Zhangzhou, Guangdong Heyuan, Liling, Shaoxing, Changxing, Pinghu, Negeri Sembilan, Malaysia, and energy-saving glass bases in Liling, Guangdong Heyuan, Changxing, Shaoxing, Malaysia and Tianjin. Silica sand (common sand and ultra-white sand) mines have been built in other production bases. At present, The company's float glass production capacity supply 1.

(2) Fuel advantage. Some of the company's production lines use natural gas + heavy oil + petroleum coke mixed combustion, which can adjust the fuel ratio according to price fluctuations, thereby reducing the fluctuation of glass production costs. Taking Zhangzhou base as an example, the proportion of the three is 3:2:5 respectively, the proportion of petroleum coke is relatively high, and the fuel cost is reduced. Comparing the pure natural gas production line with the company's mixed combustion production line, the latter has a cost advantage of 5-7 yuan/weight box due to the fuel structure.

(3) Price advantage of raw materials. The company actively laid out the upstream quartz sand reserve, and laid out the quartz sand production capacity in Zhangzhou base, Liling base, Chenzhou base and Heyuan base to ensure the production of quartz sand in the local production line, and reduced the cost of raw material procurement from the two perspectives of self-supply price advantage and transportation cost. In addition to the Zhejiang base, other production bases have built silica sand (ordinary sand, ultra-white sand) mines. At present, the overall self-supply ratio of quartz sand in the Group is about 70%. The self-supply price is about 40-80 yuan/ton, and the market price is about 200 yuan/ton. Self-supply of quartz sand can bring 4. The advantage of self-supply of quartz sand of Qibin Group can reduce the cost. 2.

Leading enterprises have the advantage of collecting raw materials. Generally, the price of soda ash is about 10% lower than market price. When the price of soda ash is 2700 yuan/ton, the cost of soda ash required by leading enterprises for glass production is 2.73 yuan/weight box lower than industry level; In the case of soda ash price of 2200 yuan/ton, the cost of soda ash required by leading enterprises for glass production is lower than industry level. 2. In recent years, the company has also made breakthroughs in deep processing and high-end glass plate, constantly improving the core competitiveness of the company. The company has established energy-saving glass bases in Liling of Hunan, Heyuan of Guangdong, Changxing of Zhejiang, Shaoxing of Zhejiang, Negeri Sembilan of Malaysia and Tianjin; in addition, the company has also established electronic glass production bases in Liling of Hunan and new neutral borosilicate medical glass production bases in Chenzhou of Hunan and Zhangzhou of Fujian.

Qibin has two main advantages in the production of photovoltaic glass. First, the company adopts 1200t/d large kilns, and the average scale of kilns is leading in the industry. The energy consumption per ton of large kilns is lower, and the cost of natural gas is lower than that of 100-ton kilns. After calculation, the cost per square meter of 3.2mm glass is expected to decrease by 1. Second, the company has planned ultra-white quartz sand bases in Hunan, Yunnan and Malaysia in advance, and the cost is expected to decrease by about 0.

3. In 2021, the company's revenue reached 25 billion 82 million, an increase of 58.65% over the same period last year; Net profit of 9.448 billion yuan, an increase of 74.2022, affected by weak downstream demand, glass prices continued to decline, short-term pressure on the company's performance, in the first half of 2022, the company's revenue of 12.028 billion yuan, an increase of 4.77%; The net profit attributable to the parent company was 2.826 billion yuan, a decrease of 36.

Xinyi Glass mainly produces float glass sheets, accounting for 67% of its performance in 2021. In addition, the company also owns automotive glass and building deep processing glass products. The gross profit rate of the company's original film business was greatly affected by the market price. In 2021, the industry was booming, and the gross profit rate of the company's float film reached 53.8%. In the first half of 2022, it fell back to 34.

(1) The original business

of Xinyi Glass is in the Pearl River Delta (Shenzhen, Dongguan, Pengjiang, Guangdong), Yangtze River Delta (Wuhu, Anhui, Zhangjiagang, Jiangsu), Bohai Rim Economic Zone (Tianjin, Yingkou, Liaoning), Chengdu-Chongqing Economic Zone (Deyang, Sichuan) and Beibu Gulf Economic Zone (Beihai, Guangxi and Chengmai, Hainan) have established large-scale domestic production bases, actively promoted business globalization and global strategic layout, and established large-scale overseas production bases in Malacca, Malaysia, with a total capacity of 2. The second line of Tianjin, the first line of Wuhu, the first line of Jianghai, the second line of Pengjiang and the second line of Hainan are in the state of cold repair, and the production capacity is 2.

Compared with the average level of the industry, the cost advantage of Xinyi Glass in the float glass business is about 15 yuan/weight box, and the net profit of 5 yuan/weight box can still be maintained at the low point of the industry. The cost advantage mainly includes the following aspects: (1) Location advantage. Like Qibin Group, most of the production capacity of Xinyi Glass is located in the southeast coastal areas, some of its bases have their own terminals, and the transportation cost of raw materials is lower than that of other enterprises. The company's original film production area is concentrated in East and South China and other economically developed areas with strong demand for glass, and the market price is higher than national average price. Taking the price on February 2 as an example, the national average price is 1660 yuan/ton, and the prices in East China and South China are 1751 yuan/ton and 1843 yuan/ton respectively, which are 5.48% and 11.0% higher than national average price, about 4.5 yuan/weight box and 9.

(2) Production line scale advantage. With the improvement of glass production process and the trend of large-scale furnace, the energy consumption per ton is reduced, and the fuel consumption required for glass production is reduced. Xinyi glass kilns account for a high proportion, with an average kiln scale of 763t/d, which is higher than average kiln scale of 676.92t/d of Qibin Group and higher than industry average level of 544. For example, the natural gas consumption per ton of Xinyi 900t/d production line is 159.7 cubic meters. The natural gas consumption per ton of Yingxin 550t/d production line is 171. If the price of natural gas is 4.5 yuan/cubic meter, the production cost can be reduced by 2.

(3) The price advantage of fuel and materials. The company is one of the few enterprises in the industry that use natural gas in all production lines. Due to the scale advantage of the company, there is a large and stable demand for gas every year. It cooperates with relevant companies in pipeline construction and enjoys the price advantage of pipeline direct gas supply. If calculated according to the price advantage of 0.5 yuan/cubic meter, the fuel cost advantage is 4. Xinyi Glass also has the price advantage of raw material collection. Generally, the price of soda ash is about 10% lower than market price. When the price of soda ash is 2700 yuan/ton, the cost of soda ash required by leading enterprises for glass production is 2.73 yuan/weight box lower than industry level; When the price of soda ash is 2200 yuan/ton, The cost of soda ash required by leading enterprises for glass production is 2.

Xinyi Glass has a number of joint ventures. Xinyi Solar Energy is the leading enterprise of photovoltaic glass in China, with photovoltaic glass production capacity by the end of 2022. 1. As the industry leader, Xinyi Solar Energy has grown rapidly by virtue of its leading product yield, advanced production lines and excellent management capabilities, and its profitability is significantly higher than industry average. It can still maintain a gross profit margin of 25% -30%. The company has more than 10,000 t/d of reserve capacity under construction in Jiangsu, Anhui, Yunnan, Malaysia and other regions, and the company's capacity scale will continue to increase in the future.

浙公网安备33010802003254号

浙公网安备33010802003254号