In 2022, after the rise in energy prices brought about by the war between Ukraine and Russia, the importance of renewable energy in various countries has been greatly increased, and the photovoltaic market is booming. In 2022, the global demand for modules is as high as 280GW, which is an astonishing growth rate of 56.5% compared with 2021. InfoLink estimates that global demand will grow by 21.6% to 338 GW in 2023, driven by the continued energy transformation in various countries. The global market growth rate in

2023 will be smaller than last year, because in addition to the higher base period, the reason why the global photovoltaic market in 2022 can achieve unexpected growth is mostly due to the impact of the Ukrainian-Russian war and soaring energy prices, which have greatly stimulated the demand for renewable energy, if there is no similar sudden major impact this year. I am afraid it will be difficult to achieve the same growth as last year. Looking closely at the markets of various countries, we will find that many countries with large markets are facing policy difficulties this year, such as the poor import conditions caused by the Xinjiang Act of the United States and the BCD tariff of India, and the introduction of grid usage fees by Brazil for small distributed projects. Policy changes will make it difficult for the growth of the global photovoltaic market in 2023 to maintain last year's growth rate. Overall, even if the growth rate declines compared with last year, it is still expected that the overall market demand will grow by about 60GW in 2023, and if countries can break through the policy restrictions, there will be opportunities for further growth in demand. Under optimistic circumstances, it is expected that global demand will have the opportunity to grow to 398GW.

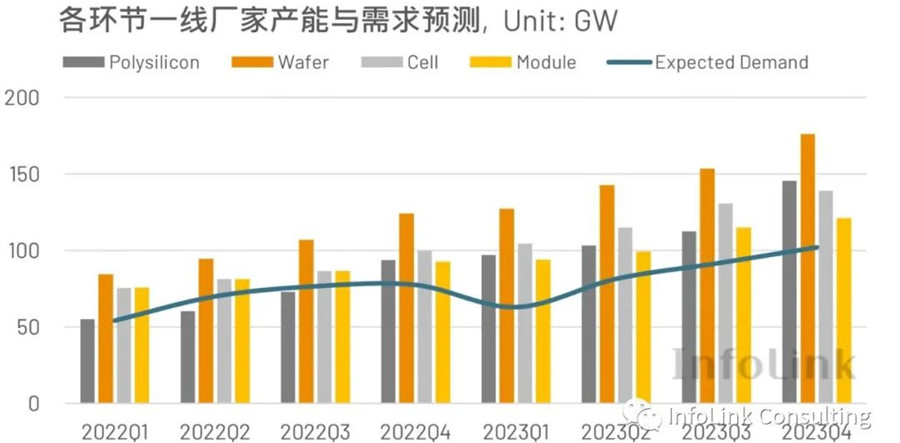

Compared with the growth of demand side, the expansion of the overall supply chain capacity is relatively significant. In 2022, there was a serious shortage of silicon materials. At the beginning of the year, the total production capacity was only 294 GW, which was seriously tight compared with the demand of 280 GW. The shortage of silicon materials also made the overall supply chain price at a high level last year. However, by the fourth quarter of 2022, the large-scale expansion plans of silicon manufacturers have come to the ground one after another, with production capacity exceeding 500GW at the end of 2022, and the volume of silicon output has also made the overall supply chain price significantly loose at the end of last year, with the prices of silicon materials and silicon wafers falling far more than expected, and the price of components falling with the upstream price. From 0.265 USD/W (2 RMB/W) in early November 2022 to 0.235 USD/W (1.8 RMB/W) in mid-January 2023.

According to the current expansion plan, the overall supply chain will be in a situation of overcapacity in 2023, and the total capacity of each link will exceed 800GW by the end of 2023, among which the capacity of the first-line manufacturers alone will be enough to meet the demand, and the increase of concentration may lead to the difficulty of maintaining the market share of the second-and third-line manufacturers in the off-season. The competition among manufacturers will become more and more fierce, and the vertical integration layout of leading enterprises and overseas expansion plans will also greatly affect the competition pattern. At the same time of large-scale production expansion of silicon materials to components, attention should also be paid to the supply of auxiliary materials such as quartz crucibles used in crystal growth and POE film of double-sided components, which may not be able to keep up with such large-scale production increase in the peak demand season, resulting in temporary shortage.

Breakdown of quarterly demand changes, the first quarter of Europe, China are the traditional off-season, especially in the European market at the end of last year due to inventory accumulation led to a significant weakening of the pull force, the impact may continue to the beginning of this year; In the past, India, which was affected by the local fiscal year and pulled a large number of goods at the beginning of the year, also saw the market shrink rapidly because of the BCD tariff, which made the global market relatively cold in the first quarter. Since the second and third quarters, with the continuous decline of supply chain prices, it is expected that demand will gradually pick up, until the end of the year, China will see another large-scale grid-connected tide due to the decline of component prices, driving demand to the peak of the whole year in the fourth quarter. In terms of

price changes, although manufacturers may adjust the operating rate to cause short-term price fluctuations, the annual price trend still shows a significant decline due to the impact of excess supply. InfoLink estimates that the average annual component price in 2023 is about 0.214USD/W (1.673 RMB/W). Compared with the average 0.266 USD/W (1.929 RMB/W) in 2022, there is a significant decline. Last year, many large-scale projects were restrained by high prices, manufacturers chose to delay the installation schedule, the annual centralized installation in the United States decreased by about 37% compared with 2021, and the rush to install ground type in China at the end of the year was not as obvious as before. In 2023, as the overall supply chain price falls, the delayed projects will start this year, and stimulate the centralized market which was relatively weak last year, further boosting the overall demand.

Compared with the shortage of supply and demand in 2022, the photovoltaic industry will gradually turn to oversupply in 2023, which will lead to a decline in prices, which is conducive to short-term demand expansion. Overall, the market will remain optimistic next year, but there are still many uncertainties. In terms of policy, India and the United States must find a solution to the contradiction between protecting local production capacity and developing the market; the European market may also face the impact of overall economic changes on demand next year, and the measures proposed for forced labor may also affect photovoltaic development in the future; The lifting of the epidemic situation in China and the change of industrial competition pattern may lead to short-term and substantial changes in supply. In the long run, with the promotion of energy transformation by governments and the approaching deadline of policy objectives, the market size will continue to grow.

浙公网安备33010802003254号

浙公网安备33010802003254号