Since November last year, Zhengzhou soda ash futures have shown a bright performance, with prices showing a unilateral upward trend and reaching a high since May last year. The strong reality is the main reason for the rising price of soda ash futures. The low inventory of soda ash, sufficient orders, and the slowdown of the cold repair rhythm of downstream float glass (1582, -1.00, -0.06%) jointly promote the rising price of soda ash. Looking forward to the future market, the current soda ash industry chain is in a low inventory state. Before the large-scale new production capacity is implemented, the low inventory state of the industry chain is expected to be difficult to improve significantly, and the future soda ash futures price is expected to maintain a high level of operation.

From the perspective of capacity, 1.2 million tons of new capacity was originally planned to be put into production in the second half of 2022, but due to various reasons, most of the plans were postponed, and the actual production was far less than expected. In the first half of 2023, the soda ash market or the situation of tight supply will be maintained, and the new production capacity of soda ash will be put into operation in the second and third quarters, of which the first 5 million tons of yuanxing Energy Project will be put into operation in four batches, and the first 1.5 million tons will be tentatively put into operation in May. Before the yuanxing Energy Trona Project is put into operation, the new production plan of soda ash is only 200000 to 400000 tons. The promotion of soda ash supply is very limited.

Source: Longzhong Information Ruida Futures Research Institute

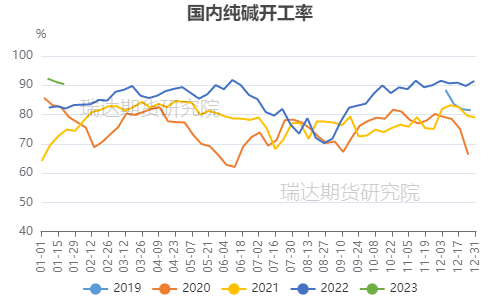

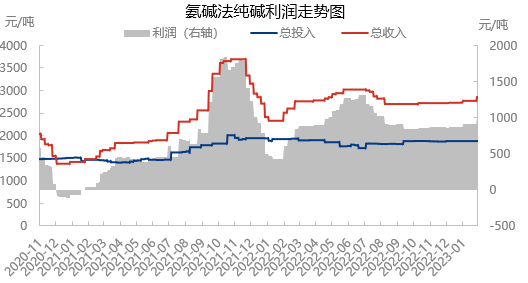

According to the operating situation of stock capacity, after the maintenance season, the operating rate of soda ash quickly returned to a high level of more than 90%. According to the statistics of Longzhong Information, as of February 2, the capacity utilization rate of China's soda ash enterprises was 91.72%, up 0.67% annually. Before the festival, individual enterprises stopped for a short time and gradually recovered during the holidays, but the start-up has not yet been normal, other units have basically stabilized, and the focus of start-up has moved up. It is understood that there is no obvious maintenance plan for soda ash enterprises in the near future, excluding sudden failures and other factors, the overall focus of soda ash start-up in February is still at a high level. In terms of profit, according to the calculation of Longzhong Information, as of February 2, the theoretical profit of domestic soda ash by ammonia-soda process was 990 yuan/ton, an increase of 8.79% compared with last week; the theoretical profit of soda ash by combined soda process (double tons) was 1913.6 yuan/ton, an increase of 5.34% compared with last week. At present, the profitability of soda ash manufacturers is good, orders are sufficient, and high profits boost the enthusiasm of manufacturers to start, but the current capacity utilization rate is close to maximization, and it is difficult to significantly improve the follow-up.

Data source: Longzhong Information

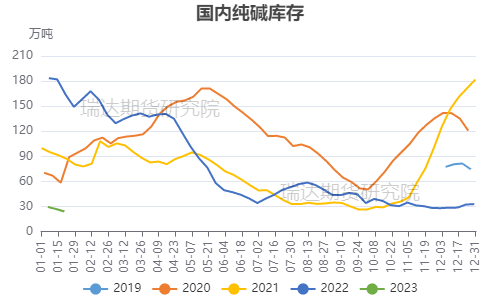

Orders are sufficient, and the inventory of soda ash enterprises is at a new low

in recent years. From the inventory point of view, Longzhong data shows that as of the week of February 2, the domestic soda ash inventory was 316,700 tons, down 8.47% from the previous month. Due to the significant increase in exports in 2022 compared with previous years, the continuous production of photovoltaic has brought about an increase in demand, and the high inventory of soda ash has been gradually digested. At present, the soda ash industry chain is in a low inventory state, and the cumulative volume of the Spring Festival this year is about 150000-200000 tons, mainly due to the limited logistics transportation during the Spring Festival, especially the automobile transportation. After the festival, with the gradual recovery of shipments and the fulfillment of orders, the inventory has declined again. The low inventory state of the industrial chain is expected to be maintained until the project of yuanxing Energy is put into operation. The future market needs to focus on the regional supply and demand changes of soda ash.

Source: Longzhong Information Ruida Futures Research Institute

Downstream glass profit repair led to an increase in production lines, boosting the demand

for soda ash. Affected by rising costs and lower spot prices, most glass enterprises have been in a state of profit loss since mid-2022. In addition, the enterprise itself has a long kiln age, and more enterprises have the demand for cold repair. However, with the intensive introduction of real estate policies, real estate expectations have been reversed. Since January, the price of float glass has risen and the profit has improved. The production line originally planned for cold repair has been postponed, while the plan for the resumption of ignition production has increased. The decline in daily melting has slowed down significantly, and the cold repair of float glass is expected to decline. If the glass profit is quickly repaired in the later period, the ignition production line will be more than cold repair production line, which will increase the demand for soda ash.

Photovoltaic glass has many ignition plans, which brings incremental

demand for soda ash. Photovoltaic power generation is an environmentally friendly renewable resource. With the continuous progress of photovoltaic power generation technology and the continuous reduction of cost, photovoltaic power generation has become one of the main renewable energy sources. From 2021 to 2022, the relevant departments of the state issued a series of policies to support the development of the photovoltaic industry, which greatly promoted the development of the photovoltaic industry in China. Photovoltaic glass, as an important component of the photovoltaic industry, is also supported by favorable policies. In 2022, the expansion of domestic photovoltaic glass production was accelerated, and more new production capacity was added. Photovoltaic glass almost doubled from 4.2 w daily melting at the beginning of last year to nearly 8 w daily melting at present, especially in the second half of last year, more photovoltaic glass devices were installed.

At present, the demand for PV in the terminal market is still high, the output of downstream product modules is expanded, and there are still many new modules in 2023, so the overall demand side is still good. 2023 is still a big year for the expansion of photovoltaic glass production. At present, there are many projects under construction/proposed. If the policy permits, the possibility of photovoltaic glass projects landing and putting into operation is higher, and the decline of silicon materials in the early stage leads to the expected increment of subsequent downstream start-up, which has a certain demand for photovoltaic auxiliary materials. According to the data of Longzhong Information, with the support of downstream consumption, the capacity utilization rate of photovoltaic glass in 2023 is expected to increase compared with that in 2022, and the capacity of photovoltaic glass in 2023 is expected to reach 110,000-120,000 tons per day. On the whole, the follow-up photovoltaic ignition plan is still more, in the context of the prosperity of the photovoltaic plate, the demand increment of photovoltaic glass for soda ash is expected to continue.

Overall, the domestic soda ash industry will re-enter the capacity expansion cycle this year, but the impact of new capacity will be concentrated in the second half of the year. At the near end, the high profit promotes the operating rate of soda ash plant to be at a high level, but at present, the utilization rate of production capacity is close to maximization, and it is difficult to improve significantly in the follow-up. On the demand side, with the intensive introduction of real estate policies, real estate expectations have been reversed, float glass profits have improved, the production line originally planned for cold repair has been postponed, and the ignition resumption plan has increased. If the glass profit is quickly repaired in the later period, the ignition production line will be more than cold repair production line, which will increase the demand for soda ash. In addition, there is still a large incremental space in the photovoltaic market, and there are still many follow-up photovoltaic ignition plans. Under the background that the prosperity of the photovoltaic sector remains unchanged, the incremental demand for soda ash in photovoltaic glass is expected to continue. At present, the soda ash industry chain is in a low inventory state, and the low inventory state of the industry chain is expected to be difficult to improve significantly before the landing of large-scale new production capacity, and the future soda ash futures price may maintain a high level of operation.

浙公网安备33010802003254号

浙公网安备33010802003254号