near future are mainly those with net inflow of population and talents, rapid inventory depletion and prominent industrial advantages, while those without prominent industries, population outflow and high inventory have relatively poor recovery performance. Cities in the first echelon of

recovery: Beijing, Shenzhen, Chengdu, etc. The three cities grew positively for three consecutive months on a month-on-month basis and improved year-on-year for three consecutive months.

Recovery of the second echelon cities: Shanghai, Guangzhou, Suzhou, Hangzhou, Nanjing, Wuhan, Qingdao, Wuxi, Foshan, Ningbo, etc. These cities have achieved positive growth for two months or three consecutive months. Cities with weak

recovery: Fuzhou, Nanning, Quanzhou, Liuzhou, Wuhu, Loudi, Ji'an, etc. These cities have small month-on-month and year-on-year improvement and short duration.

With the further implementation of the real estate relaxation policy and the gradual recovery of confidence in buying houses, we believe that the property market will continue to maintain a weak recovery in 2023, with the recovery focusing on second-hand housing and improved housing in hot cities. It is expected that the sales area of commercial housing will stabilize and return to positive in 2023, with a year-on-year growth of 5%.

In the long run, regional differentiation is the biggest feature of the future real estate market; the development era of general rising housing prices is over, and the differentiation of the real estate market within the city is intensified; industry + location is king; the era of improvement is coming, and product strength will become the core competitiveness . The key to the sustained recovery of the

housing market lies in the recovery of market confidence, supply clearance and sales repayment. To solve the real estate problem sooner rather than later, the current real estate market has not yet come out of the predicament, the risk has not been lifted, it is suggested to resolve the real estate industry dilemma as soon as possible. Seven measures can be considered: lowering the down payment ratio of the second suite to support improved demand, lowering the interest rate of the first suite loan to support the first set of rigid demand, giving appropriate subsidies to the rental expenditure of low-income families and fresh graduates, liberalizing the restrictions on the purchase of the first set of non-local houses in second-tier cities, reducing transaction taxes and fees, changing the previous strict measures of restricting purchase, lending and price, and returning to normal market conditions. Support banks to reduce the interest rate of stock mortgage loans, "transfer with mortgage" and other convenient and good governance. At the same time, through the construction of new models such as "urban agglomeration strategy, human-land linkage, financial stability, rent and purchase simultaneously", we can promote long-term stable and healthy development.

Contents

1 National recovery: Xiaoyangchun in the first quarter, the recovery slowed down in April, and the second-hand housing market was better than new housing market

. 2 City recovery: Differentiated recovery, the first and second tier cities were better than third and fourth tier cities

. 3 Short-term outlook: Continue the dotted recovery trend. It is estimated that the sales of commercial housing in 2023 will increase by 5%

compared with the same period last year. 4 Long-term outlook: metropolitan agglomeration, intensified regional differentiation, "industry + location" is king, and the era of improvement is coming

. 5 Enlightenment: short-term city-specific policies are moderately relaxed. Establishing a long-term mechanism

such as linking people and land Text

1 National Resumption: Xiaoyangchun in the first quarter, the recovery slowed down in April, and the second-hand housing market was better than new housing

market in the first quarter of 2023. With the further landing of the real estate relaxation policy, the recovery of the confidence of buyers, and the concentrated release of the real estate backlog demand, the real estate market ushered in a partial Xiaoyangchun, and the sales ring ratio turned positive and improved significantly year on year. In April, sales turned negative, the decline was higher than same period in 2019-2022, the year-on-year increase was narrower than in March, and the recovery process slowed down slightly.

From the perspective of new housing sales, new housing sales bottomed out in the first quarter, first-and second-tier and third-and fourth-tier cities were divided, and the ring-to-ring decline in April was higher than same period in previous years, and the recovery was weaker. In the first quarter of

2023, 422,000 new housing units were sold in 49 sample cities, with a growth rate of 8.6% compared with-15.0% in the fourth quarter of last year, a decrease of 6.2% compared with the first quarter of 2022, and an average turnover of 56. The growth rates of first-tier, second-tier, third-tier and fourth-tier cities all changed from negative to positive, increasing by 2.1%, 10.6% and 8.8% respectively; Compared with the first quarter of 2022, the growth rate of first-tier and second-tier cities increased by 10.0% and 5.0% respectively, while that of third-tier and fourth-tier cities narrowed to 41.

2023. In April, 132000 new housing units were sold, and the ring-to-ring growth rate changed from positive growth in March to negative growth, down 30.9%. Less than growth rate of + 5.3%, + 27.0%, -7.7% and -18.8% in April 2019-2022; Among them, the growth rate of first-tier, second-tier and third-tier cities has changed from positive to negative, while that of first-tier cities has increased by 123.7% year-on-year, mainly due to the low turnover base in Shanghai last year. The second and third lines decreased by 3.4% respectively. 34.

year, Second-hand housing transactions in 18 sample cities amounted to 240000 units, with a ring-to-ring growth rate of-14.6% in the fourth quarter of last year to 40.5%, a substantial increase of 70.8% in the first quarter of 2022 compared with the same period last year, and a significant increase over the average of 17 in the first quarter of 2019-2021. 45.9%, 39.7% and 27.7% respectively; Compared with the average number of transactions in the same period in 2019-2021, the number of transactions in the first-tier and second-tier cities increased by 8.7% and 49.2023

, respectively. In April 2023, the number of second-hand housing transactions decreased by 21.3% annually, and the growth rate changed from positive to negative in March. Compared with the performance of + 27.0%, + 37.9%, + 2.0% and -4.2% in April 2019-2022, the year-on-year growth rate was 68.8%, which was higher than that in March. Among them, the month-on-month growth rate of first-tier, second-tier and third-tier cities changed from positive to negative compared with that in March, and the year-on-year growth rate narrowed to varying degrees compared with that in March.

year, The sales amount of the top 100 real estate enterprises was 1.8 trillion yuan, turning from negative to positive year-on-year, with an increase of 8. The number of real estate enterprises whose cumulative sales increased by more than 50% year-on-year, and the number of enterprises whose sales increased by more than 30% year-on-year reached 38. In terms of echelons, the threshold of sales amount of TOP10 real estate enterprises has increased significantly year on year, while the threshold of the top 30 and 50 has been lowered, and the market share has been further concentrated to the head real estate enterprises. In April, compared with March, the sales of the top 100 real estate enterprises decreased by 17.4% from positive to negative, with a year-on-year increase of 29.1. From January to April, the sales amount of the top 100 real estate enterprises was 2.4 trillion yuan, with a year-on-year increase of 12. In terms of scale, from January to April, there were 6 real estate enterprises with sales exceeding 100 billion yuan, an increase of 3 over the same period last year; Sales of 50-100 billion housing enterprises 8, an increase of 2 over the same period last year.From the perspective of

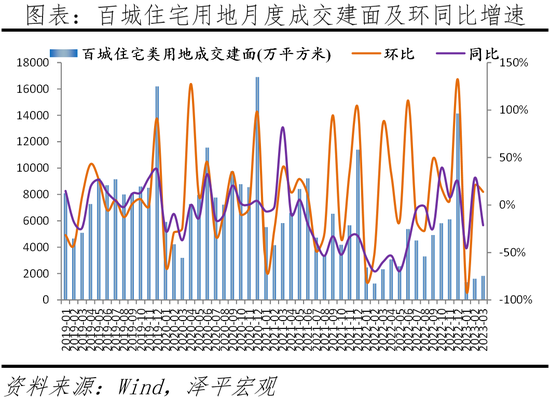

investment, in the first quarter, affected by the land supply system, the scale of land supply declined, the scale of transactions declined, but the average transaction price rose; in April, the core cities concentrated on land supply, and the heat of land acquisition rebounded. The central state-owned enterprises and private enterprises continue to differentiate, and the competition in key cities is fierce. In the first quarter of

2023, affected by the land supply system, the time of land supply in various cities was delayed and the scale of land supply declined, resulting in a decrease of 81.7% annually and 20% year-on-year in the construction area of residential land in 100 cities. The average transaction price of residential land in 100 cities increased by 4.1% year-on-year, and the average premium rate increased from 3.87% in the first quarter of last year to 5. From the perspective of land acquisition by enterprises, the scale of land acquisition by top 100 real estate enterprises continued to narrow in the first quarter and from January to April, and the land acquisition among real estate enterprises and cities continued to differentiate. On the one hand, the proportion of central state-owned enterprises in land acquisition has increased, accounting for nearly half, while the enthusiasm of private housing enterprises in land acquisition is still low. According to the data of the Chinese Academy of Sciences, among the TOP50 housing enterprises in April, the central state-owned enterprises, local state-owned enterprises and urban investment, private enterprises and mixed ownership housing enterprises accounted for 44%, 15%, 28% and 11% respectively. On the other hand, the heat of land acquisition by real estate enterprises in different cities is obviously differentiated. The competition in hot cities such as Hangzhou and Hefei is fierce. The first batch of centralized land supply in Hangzhou is sold within one hour, while in cities with lower heat such as Changchun, most of the plots are sold at the bottom price.

is: 0HTM L0 UNK5 first-and second-tier cities are better than third-and fourth-tier cities, the second-hand housing market is better than new housing market, and the demand for improvement is stronger than rigid demand. 0 HTML 0 UNK6 The cities with better recent recovery are mainly those with net population inflow, rapid inventory depletion and prominent industrial advantages, while the cities without prominent industries, population outflow and high inventory have relatively poor recovery performance. 0HTML0UNK7 First, on the demand side, the total population and structure affect the demand for housing. 0 HTML 0 UNK8 The top five cities in terms of permanent population growth in the past year are Changsha, Hangzhou, Hefei, Xi'an and Nanchang, with a population growth of more than 100,000. In terms of structure, the younger cities are Shenzhen, Dongguan, Xiamen, Foshan, Guangzhou and Zhengzhou, with less than 10% of the population aged 65 and over, while Nantong, Yantai, Chongqing and Dalian account for more than 15% of the aging population. The cities with large net inflow of talents are Beijing and Shanghai. Although the growth rate of permanent population in the two cities has changed from positive to negative due to strict population control, there is still a large net inflow of middle and high-end talents. 0HTML0UNK9

Why is the recovery of Fuzhou property market cold? In 2022, the permanent population of Fuzhou increased by 28000 people, compared with the major cities in the country, the population growth is relatively small, even lower than that of Quanzhou. 2. Although Fuzhou launched a series of policies to support the development of the real estate market in 2022, such as taking the lead in liberalizing the purchase restrictions in March last year, lifting the purchase restrictions in an all-round way, non-registered population can buy houses in urban areas without social security. However, due to the relatively fatigue development of high-end industries, the policy of relaxing purchase restrictions is not enough to stimulate the growth of housing demand.

3 Short-term outlook: The dotted recovery trend continues, and the sales of commercial housing is expected to increase by 5%

in 2023 compared with the same period last year. At present, with the implementation of a series of measures introduced by the state to stabilize the real estate market, the darkest moment of real estate has passed and the recovery channel has been opened. The real estate market has not yet fully recovered, the confidence of the industry has not yet been fully boosted, there is still a certain gap between the transaction of the real estate market and the level of the same period in 2019-2021, the recovery foundation is not solid, the market should not be blindly optimistic, substantive and effective measures are needed to promote the continuation of the recovery of the real estate market, and to boost market confidence on the premise of adhering to the principle of "no speculation in housing". This is related to the process of China's economic recovery and the resolution of real estate financial risks. With the further implementation of the previous real estate policy, the continued relaxation of the follow-up real estate policy and the gradual recovery of confidence in buying houses, it is expected that the real estate market will continue to maintain a weak recovery trend in 2023, with the recove ry focusing on second-hand housing and improved housing in hot cities. China's Real Estate Market Outlook

in 2023: Can It Be Saved This Time?

On the demand side, the peripheral areas of first-tier cities and the core areas of major second-tier cities relaxed purchase restrictions due to the implementation of city policies, residents'wait-and-see mood reversed, and sales increased significantly. On the supply side, the favorable policies on the financing side of high-quality real estate enterprises increased, landing quickly, the confidence of real estate enterprises accelerated to recover, and the enthusiasm for land acquisition increased . We expect that the sales area, completed area and investment in real estate development of commercial housing will stabilize and return to positive in 2023, with a year-on-year increase of + 5%, + 6% and + 2% respectively; Considering the factors such as less land acquisition in 2022, It is estimated that the area of new construction in 2023 will be -7.4 compared with the same period last year.

Long-term outlook: metropolitan agglomeration, intensified regional differentiation, "industry + location" is king, and the era of improvement is coming

. We have estimated the real estate market in the next ten years, taking into account the urbanization process, the demand for improvement, urban renewal, etc. China's real estate market still has room for future development. According to our calculation, the annual average new urban residential demand in 2023-2032 is about 1.09 billion square meters, compared with the annual average new urban residential demand in 2011-2022, the total residential demand in China will drop to 1 billion square meters in 2032. In 2023, China's new urban residential demand will be about 1.2 billion square meters per year, and the increase of urban permanent population (excluding the change of administrative divisions), the improvement of living conditions and the demand for urban renewal will account for 31.5%, 32.7% and 35. The increase of urban permanent population, the improvement of living conditions and the demand for urban renewal account for 15.4%, 37.4% and 47% of the total demand, respectively. The total and proportion of the demand for improvement show an increasing trend year by year, and it is expected to surpass the demand brought by the growth of urban permanent population and become the largest demand after 2023.

We believe that the future of real estate has the following trends:

First, regional differentiation is the biggest feature of the future real estate market. There are three specific performance: First, the eastern coastal areas of real estate development potential better than northeast and western regions, the southern region of the real estate market as a whole better than northern region; Second, the real estate growth potential of developed urban agglomerations and metropolitan areas is higher than that of underdeveloped urban agglomerations and underdeveloped metropolitan areas, and the real estate market performance of underdeveloped urban agglomerations and underdeveloped metropolitan areas will be better than that of non-urban agglomerations and non-metropolitan areas; third, the real estate market differentiation of first-tier cities, strong second-tier cities with population inflow and third-tier and fourth-tier cities with population outflow. According to our previous research results, the ratio of households in a mature market in a country is generally 1. In 2020, the number of cities with a ratio of more than 1.1 in China has reached 56. We predict that 70% of the cities in China will have a surplus of houses in the future, and only 20% of the cities have potential houses.

Second, the era of general inflation in cities is over, and "industry + location" is king. From 1978 to 2022, the ratio of urban households in China increased from 0.8 to 1. From the perspective of policy, since 2016, with the proposal of "no speculation in housing" and the deepening of city-specific policies, cities have increased the frequency and fineness of real estate regulation based on local conditions. From the perspective of environment, China's population began to grow negatively in 2022, and the total fertility rate fell below 1. Real estate entered the stock era from the era of large-scale development. Firstly, historical accumulation creates "lots" in old urban areas, urban planning and development create new "lots", and "lots" affect real estate value by attracting people with high purchasing power. Secondly, industrial agglomeration affects the development of real estate in the plate by creating people with high purchasing power and affecting land costs, and industrial spillover will drive the development of real estate in the surrounding plate.

Third, with the advent of the era of improvement, product strength will become the core competitiveness . The era of housing shortage in China as a whole has passed, and consumers'pursuit of housing has changed from "having a house to live in" to "living in a good house". Everyone has a house to live in, which does not mean that everyone has a good house to live in. Residents have a higher demand for housing quality. The difference of housing product strength promotes the differentiation of housing value. In terms of household type, "improvement is king" represents that the demand for improvement is becoming the mainstream, the proportion of three-room units is increasing, the proportion of four-room units is also increasing, and the demand for two-room units is declining year by year. With the growth of per capita housing area, consumers will change from "living in small houses" to "living in big houses", and large apartments may gradually become the mainstream of house purchase in the future. In terms of quality, the quality of housing affects the value of housing, the demand for housing consumption has changed from "having a house" to "living in a good house", and the residents'demand for housing quality has increased.

Four, the industry is clear and the surplus is king. Pure development of housing enterprises to "light and heavy" transformation. The era of high leverage is over. The real estate industry is transforming to high-quality development, most of the development-oriented housing enterprises will disappear in the future, and the market share of the leading housing enterprises will be further increased. With the liquidation of the industry and the end of the "three high" business model, the overall debt ratio of the industry will decline. After the cold winter of the industry, more and more housing enterprises began to explore new development models, improve cash flow safety cushion, and will transform to the new development model of "light and heavy" in the future.

5 Inspiration: Short-term city-specific policies are moderately relaxed, and long-term mechanisms

such as linking people and land are established. At present, it is not simply to rescue the housing market in the traditional sense, but to stabilize the housing market while giving full play to its real economic attributes and avoiding the resurgence of its financial attributes. In 2020, real estate and its industrial chain accounted for 17% of China's GDP (full contribution), of which the added value of real estate industry accounted for 7.3% of GDP (direct contribution), and the industrial chain driven by real estate accounted for 9% of GDP. It can also promote the stability of the real estate market through short-term measures, and promote the healthy development of the real estate market through the construction of new models. Stabilize the real estate market

in the short term: adhere to the principle of "no speculation in housing", and moderately loosen the restrictions according to the city to promote the soft landing

of real estate. On the premise of "no speculation in housing", cities should implement policies according to the city and moderately loosen the restrictions to promote the soft landing.

1) Appropriately lower the threshold of purchase restriction in population inflow areas and enhance market confidence.

2) Reduce the down payment ratio of the first set and the improved second set to reduce the down payment pressure of the people who just need it and the people who buy the improved house.

3) Lowering the interest rate of the first and improved housing loans and speeding up the approval of loans.

4) Increase the loan limit of the provident fund or allow the withdrawal of the balance of the provident fund not included in the calculation of the loan limit to pay the down payment.

5) Beijing, Shanghai, Guangzhou and Shenzhen should appropriately lower the threshold for settling down and purchasing houses, and fully respect the objective law of population and industry gathering in metropolitan areas.

6) Resolve the risks of real estate enterprises through loan extension, debt restructuring, mergers and acquisitions, etc.

Long-term mechanism: Promote the reform

of housing system with urban agglomeration strategy, human-land linkage, financial stability, real estate tax and simultaneous rent and purchase as the five pillars. It is suggested that a long-term housing system should be constructed with the five pillars of urban agglomeration strategy, human-land linkage, financial stability, real estate tax and simultaneous rent and purchase.

1) Promote the strategy of urban agglomeration in metropolitan area. People go with the property, and people go up. The report of the 20th National Congress pointed out that the strategy of coordinated regional development, major regional strategies, the strategy of main functional areas and the strategy of new urbanization should be implemented in depth.

2) Take the increment of permanent population as the core to reform the "human-land linkage" and optimize the land supply. Promote the linkage between new permanent population and land supply, the balance of cultivated land occupation and compensation across provinces and the increase and decrease of urban and rural land use, strictly implement the principle of "linking inventory cycle with land supply", and optimize the current land supply mode.

3) Maintain the long-term stability of monetary policy and real estate financial policy. Stabilize the expectations of home buyers and support the demand for rigid demand and improved housing. Standardize the financing use of real estate enterprises, support the reasonable financing needs of real estate enterprises, and provide a certain time window for real estate enterprises with problems to have self-help opportunities.

4) Steadily promote the real estate tax pilot. Real estate tax instead of land finance is the trend of the times. In 2021, the central government proposed to carry out the pilot work of real estate tax reform. In the future, it is necessary to establish a scientific economic model to assess the impact of real estate tax on all parties.

5) The report of the 20th National Congress of the Communist Party of China emphasizes "speeding up the establishment of a housing system with multi-subject supply, multi-channel security and simultaneous rent and purchase".

浙公网安备33010802003254号

浙公网安备33010802003254号