July, affected by the bad weather in the north, the Shahe River was flooded, the glass warehouse was flooded, and the logistics transportation was also blocked. At present, the glass factory has been able to enter and exit the warehouse normally, and the transaction situation is better. According to previous years, August and September are the peak season for purchasing glass sheets, but this year it seems that the price has risen ahead of schedule. On the other hand, the sentiment of traders is still pessimistic, the implementation of low inventory strategy, lack of purchasing enthusiasm, less warehouse stock. Especially this year, there are fewer downstream deep processing projects and more home decoration projects, and the problem of funds has not been solved. Glass futures after this round of rise, the lack of short-term upward drive, do more need to be cautious. Glass production capacity will continue to increase in the future, while the demand side will continue to be supported by the completion and delivery of buildings for a long time, and the contradiction between supply and demand may intensify. In the first seven months of

this year, the glass market fluctuated, with a long period of wide shocks and a unilateral rapid rise and fall.

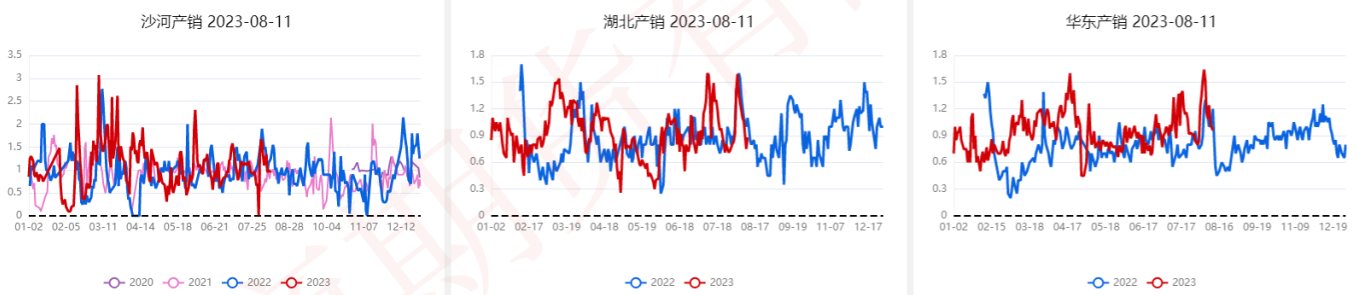

In the first stage, at the beginning of the year, the orders of glass downstream deep processing enterprises were poor, the willingness to buy the original film was not strong, and the futures market fluctuated at a low level. After the festival, the production and sales of Shahe, Hubei, East China and other places began to strengthen, the downstream deep processing enterprises gradually began to replenish the original sheet inventory, the glass factory inventory began to go to the warehouse, and maintained the trend of going to the warehouse until the end of April, the spot trading sentiment rose, the glass factory gradually raised the price, pushing up the buying sentiment of traders and futures merchants. After the total inventory of the national factory warehouse was close to the historical normal level, the spot of glass factories in Hubei began to lack, the inventory of Shahe manufacturers was close to the bottom, the long futures were squeezed, and the 09 contract rose to about 2000 yuan/ton.

In the second stage, from the end of April to the end of May, the glass futures market continued to fall rapidly, mainly due to two reasons, one is the downward cost, the price of raw materials, including soda ash and coal, which led to the decline in glass production costs, the other is the poor downstream procurement of glass, the weak replenishment of deep processing enterprises, and the weakening of production and marketing. In more than a month, the 09 contract dropped rapidly from the highest point of this year to the lowest point of this year, about 1400 yuan/ton.

In the third stage, since June, the middle and lower reaches of glass have begun to replenish, production and sales have improved, and the futures market has followed the rise. Glass spot prices rose in advance before the peak season, various policies were introduced to boost confidence in the real estate market, and the northern rainstorm weather caused greater pressure on the supply side in the short term, resulting in a boom in downstream orders.

However, we believe that the rainstorm weather in the north is a short-term factor, and the rapid rise of the market is unsustainable; the price of the original glass sheet rises in advance before the peak demand season, which may overdraw part of the space to continue to rise; and the weak reality pattern of the real estate industry has not been substantially improved, the capital problem of the glass deep processing enterprises is still there, and the new orders are insufficient. Therefore, the driving force for the further rise of the short-term glass market is limited, and the risk of doing more contracts in recent months is greater.

Last week, the mainstream price in North China was 1955 yuan/ton, an increase of 60 yuan/ton. The mainstream price in Central China is 2040 yuan/ton, an increase of 80 yuan/ton annually. The mainstream price in East China was 2236 yuan/ton, an increase of 64 yuan/ton. The mainstream price in South China was 2322 yuan/ton, an increase of 118 yuan/ton. In Shahe area, the safety price is 1965 yuan/ton, with a month-on-month increase of 56 yuan/ton; the Great Wall price is 1975 yuan/ton, with a month-on-month increase of 83 yuan/ton; the Jinhongyang price is 1977 yuan/ton, with a month-on-month increase of 63 yuan/ton; the Dejin price is 1915 yuan/ton, with a month-on-month increase of 57 yuan/ton; The price of jade crystal was 1920 yuan/ton, an increase of 43 yuan/ton annually. The price of Shahe glass remained basically stable, and all Shahe brands reduced their prices slightly.

Last week, the total production capacity of float glass was 61 million 344 thousand tons per year, and the ring ratio was flat. The capacity utilization rate was 81.1%, a decrease of 0.3% compared with the previous month. The production capacity was 49.75 million tons per year, a decrease of 184,000 tons per year. The daily melting capacity of float glass was 166 thousand and 600 tons, an increase of 0.1 million tons. The daily melting volume is gradually climbing, and it is expected to reach the peak of the annual daily melting volume in September or October. The production cost of float glass with petroleum coke as fuel is 1372 yuan/ton, an increase of 30 yuan/ton annually, and the profit is 668 yuan/ton, an increase of 70 yuan/ton annually. The production cost of float glass with power coal as fuel was 1571.8 yuan/ton, a decrease of 3.3 yuan/ton, and the profit was 365 yuan/ton, an increase of 64 yuan/ton. The production cost of float glass with pipeline gas as fuel was 1745.8 yuan/ton, an increase of 9.3 yuan/ton, and the profit was 486 yuan/ton, an increase of 81 yuan/ton. Shahe's production and sales were 98%, a decrease of 33%. Hubei's production and sales were 88%, a decrease of 50%. Production and sales in East China were 96%, a decrease of 68%. Last week, the production and sales data of Shahe glass were still acceptable, and the sales situation was good, but the sales situation in Hubei was weakened. In terms of inventory, the total inventory in China was 41.63 million weight boxes, a decrease of 4.08 million weight boxes on a month-on-month basis; the inventory in North China was 5.73 million weight boxes, a decrease of 930,000 weight boxes on a month-on-month basis; the inventory in Central China was 2.77 million weight boxes, a decrease of 520,000 weight boxes on a month-on-month basis; the inventory in East China was 13.96 million weight boxes, a decrease of 1.55 million weight boxes on a month-on-month basis; The inventory in South China was 5.4 million weight boxes, a decrease of 490,000 weight boxes compared with the previous month. Each region maintains destocking, and the inventory is at a low and medium level in the historical data. In Shahe area, the total weight of Shahe factory warehouse and community warehouse is 3.68 million weight boxes, with a month-on-month decrease of 560,000 weight boxes; among them, the weight of Shahe factory warehouse is 1 million weight boxes, with a month-on-month decrease of 510,000 weight boxes; the weight of Shahe community warehouse is 2.67 million weight boxes, with a month-on-month decrease of 50,000 weight boxes. The situation of Shahe River going to the reservoir is better, and the production and marketing situation of Shahe River is close to the disk.

Looking forward to the future, the glass supply side will have more new production capacity. In the remaining five months of 2023, it is planned to ignite 8 new lines, with a cumulative daily melting capacity of 6,800 tons; resume production and ignite 11 lines, with a cumulative daily melting capacity of 6,900 tons; and cold repair 14 lines, with a cumulative daily melting capacity of 9,250 tons. It is expected that the daily melting volume will reach the peak of this year in September or October this year. Therefore, the supply of float glass is expected to continue to increase and the competition in the industry will intensify. On the profit side, the profit of float glass with petroleum coke as fuel has risen to about 670 yuan/ton, and the profit of float glass with steam coal and pipeline gas as fuel is also between 350-500 yuan/ton. The high profit of the industry has led most glass factories to increase their production efforts and give priority to shipment. Once the shipment is blocked and the sales are not smooth, the willingness of glass factories to support the price may not be great. On the other hand, as a positive factor, the policy support of guaranteeing the completion and delivery of buildings is still in place for a long time, and the real estate demand for float glass has a certain rigidity. Therefore, the contradiction between supply and demand in the future will still be the main game point of the futures market.

Risk warning: The contents and opinions of this article are for reference only and do not constitute any investment advice.

浙公网安备33010802003254号

浙公网安备33010802003254号