European PPA-backed wind and PV projects : 5% -9%. Risk premium for UK clean energy investors in July

2023 (below the five-year average of 6.1% until 2022): 2.8%. Increase in the UK base rate since the beginning of

2022 (the ECB base rate has increased by 400 basis points over the same period): 475 basis points. European wind and PV investors are raising their return on equity expectations after

years of declining yields. The reversal of this trend follows a year-long period of monetary tightening, which has led to higher project debt costs. Investors are looking for higher returns, but they still don't want to lose out on investment opportunities as demand for photovoltaic and wind assets remains strong. European PV and wind investors are upgrading their target equity returns

due to rising interest rates. Bloomberg New Energy Finance interviewed 10 equity investment experts in the first half of 2023 to discuss the attractiveness of investing in onshore wind and photovoltaic in different European markets over the past six months. We explore how the risk-reward landscape has changed in each market and the impact on the target equity IRR.

The deal evidence does not yet show a clear rise in target IRR, but investors interviewed by Bloomberg New Energy Finance say the M & a market is cooling and target returns are rising. To remain competitive and improve returns, investors continue to seek early-stage projects and acquire development-stage assets. Rising

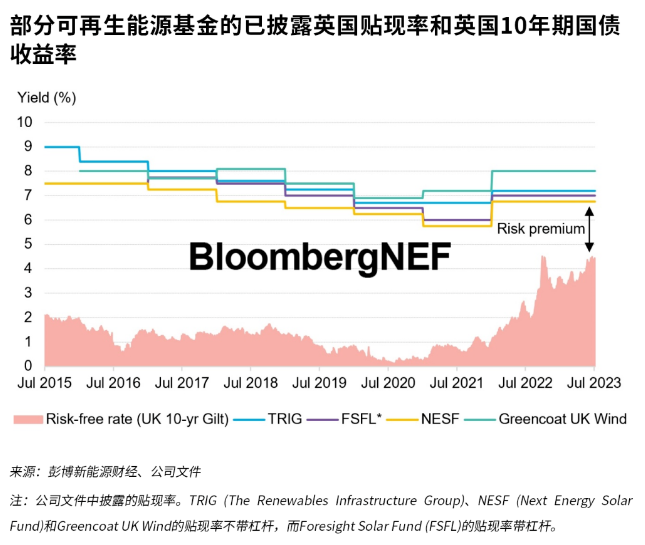

long-term Treasury yields have pushed listed closed-end PV and wind funds to increase the discount rate on their portfolios. Investors in these funds – the big asset management groups – are putting money back into bonds, causing the closed-end funds' share prices to fall, boosting yields.

While the risk-free rate has jumped in the past year, the expected return to investors has not risen by the same amount, causing the risk premium to fall. In a market with increased competition for assets, investors see little change in the discount rate.

浙公网安备33010802003254号

浙公网安备33010802003254号